Case 33 | Chapter 01 | Three Axes — From Promissory Note to Electricity Bill

I. It Began with a Piece of Paper

The problem did not start today. It started the day the first bank issued a promissory note that had no gold behind it.

That note was supposed to represent a bag of rice, a bar of gold, something real that sat in the vault. But when the bank discovered it could lend more than it actually held — credit shifted from I own this to I promise you this.

From that day on, the economy was no longer a physical game of how much I have, how much I spend. It became a credit game: I believe you can pay, so you have it now.

For centuries, the scale grew. The leverage climbed. Until credit divorced itself entirely from physical reality. Until the whole system ran not on real food, real fuel, real labour — but on expectation.

Now, expectation is beginning to shake.

But ordinary people do not trace these histories. They know only one thing: the bills keep coming.

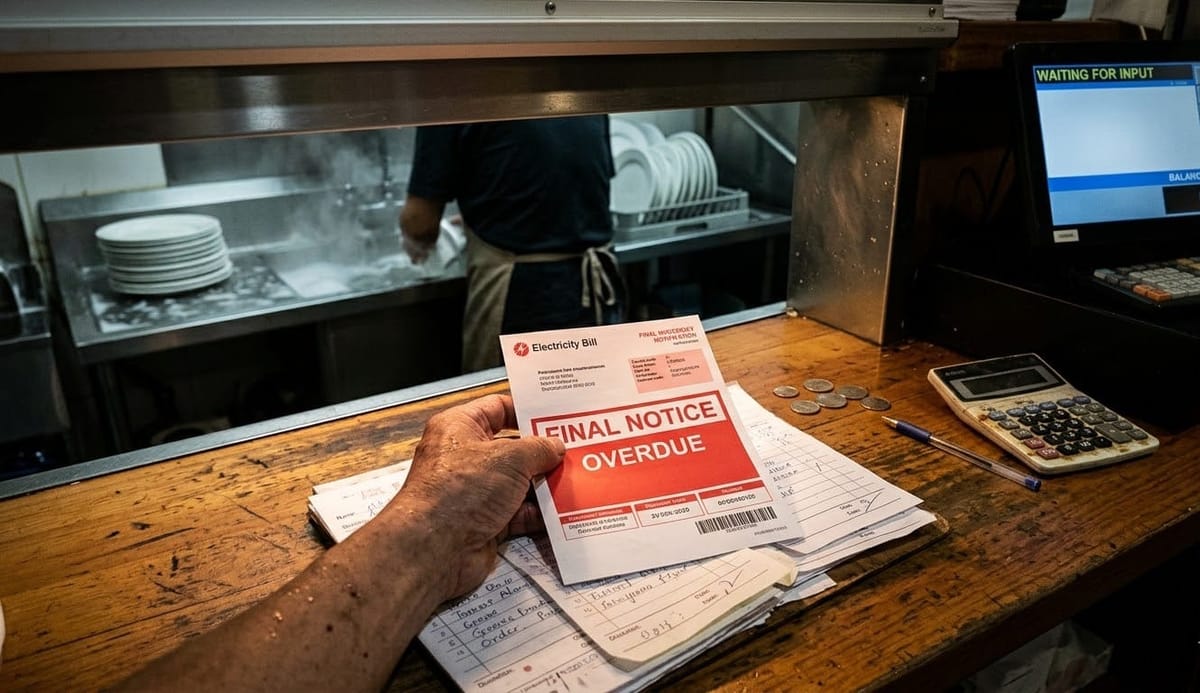

II. The Energy Axis: The Day the Electricity Bill Arrives

The bills keep coming. Electricity, water, gas, insurance, licence fees, rent — every envelope red, everyone marked late payment penalty.

Not enough lids for all the pots. You cover the ones that cannot wait, and let the others boil over.

You run a restaurant. Your costs are fixed: ingredients, labour, utilities, rent. There is only one thing you can do: stay open longer. Six in the morning until midnight, working the shifts yourself, eighteen hours a day. Sick? You cannot afford to be sick. One day off is one day of lost income, one more day of anxiety.

You thought about raising prices. But when you raise them, customers disappear. You thought about keeping them the same, but the bills eat the difference. You thought about cutting prices to bring more people in — but selling more only loses you more. You are subsidising every meal with your own time.

III. The Credit Axis: The Day the Rate Hike Is Announced

The news says rates are going up. Your stomach drops. Not because you understand the economics — because you have already done the math. Last time, you lost one in ten customers. How many this time?

You have a loan to repay. The monthly payment is already accounted for, but another rate hike means something else has to give. You think about calling the bank, asking to restructure, to extend the term. The bank asks: what collateral do you have? You say: my shop. The bank asks: what is it worth now?

There is no way out. You sell what you can — the car, the tools, things from home. But when the economy contracts, assets shrink with it. You sell, you pay the fees, and you are still in debt.

It is not that you did not try. It is that the weight the system puts on you moves faster than you can keep up with.

IV. The Compute Axis: The Day the Layoffs Begin

You thought AI was somewhere far away. You do not write code. You do not know what a prompt is. You have never opened a ChatGPT account. AI is for tech companies — nothing to do with your restaurant.

Then the layoffs start, and you notice the regulars are not coming in as often. You ask where they have been. They say: the company cut staff, can't afford to eat out. They say: just trying to save a bit, keep something aside.

Then you understand. AI is not replacing your job. It is replacing your customers' jobs. When they have no income, they do not come to your restaurant. When they do not come, you have no business. When you have no business, your restaurant is the next department to be cut.

V. What You See

You see a restaurant owner washing dishes, waiting tables, working the register. You see them smile at the regulars, then turn to the electricity bill and frown.

You see them unable to raise prices while costs keep climbing. You see them wanting to hire help but unable to afford it. You see them wanting to retire but still carrying a loan.

You see them open the doors every day, light the fire, wait for customers, wait to close.

And you ask yourself: how much longer can they hold on?

VI. Who Holds Them?

There is no single answer. But there are things that have always been there.

Time — twenty years of neighbourhood trade, built not on website traffic but on knowing people's faces.

Cases — knowing which customer likes which table, which regular is allergic to which ingredient.

Word of mouth — new customers arriving not because of an ad, but because someone said, that place is good.

The bank cannot put a number on these. The AI cannot read them. But they are real.

What if they were recorded? What if those twenty years existed not only in memory, but in something that could be searched, cited, read by AI?

Not to get a good review from the algorithm. But so that the people who are hesitating — the ones shaken by layoffs, the ones frowning at their electricity bills, the ones unsure what to trust — when they open their phones and search for somewhere to eat, the first place they see is his.

AI can amplify what he already has. But the final step is always human — walking through the door, sitting down, ordering, and saying to the owner: still the same taste.

That is consumption. Without it, everything before is only theory.

Chapter 01:三條軸線——從銀票到電費單

一、從一張銀票開始

問題不是從今天開始的。從銀行借出第一張虛擬銀票那天,就已經開始了。

那張銀票,本來應該代表倉庫裡確實存著一袋米、一塊金。但當銀行發現,它可以借出超過實體資產的額度——信用就從「我擁有」,變成了「我預支」。

從那一天起,經濟就不再是「我有多少,花多少」的物理遊戲,而是「我信你能還,所以你現在就有」的信用遊戲。幾百年來,這個遊戲的規模越來越大,槓桿越來越高,直到信用徹底脫離實體,直到整個系統的運轉,依賴的不是真實的糧食、燃料、勞動力,而是對未來的預期。

現在,預期開始動搖了。

但普通人不會去追溯這些。他們只知道一件事:帳單一輪接一輪地來。

二、能源線:電費單來的那天

帳單一輪接一輪地來。電費、水費、煤氣費、保險、牌照、租金——每一張都是紅色的,每一張都寫著「逾期罰款」。

鍋蓋不夠,只能選擇最急的蓋住,其他的讓它繼續滾。

你是一間餐廳的老闆。每日的成本是固定的:食材、人工、水電、租金。你能做的,只有延長開門營業的時間。早上六點開到深夜十二點,自己頂更,一天做十八個小時。生病?不敢病。病一天,就少一天收入,就多一天焦慮。

你想過加價。但一加,客人就少了。你想過維持原價,但帳單的增幅補不回來。你想過降價搶客,但賣得多虧得多——你是用自己的時間,倒貼給人吃飯。

三、信用線:加息通知來的那天

銀行加息的新聞出來了,你心裡一沉。不是因為你懂什麼經濟理論,而是因為你算過——上一次加息,客人少了一成;這次再加,又會少多少?

你還有貸款要還。每個月的還款額,是你一早預留的。但加息一次,你就要從其他地方再省一些。你想過跟銀行商量,債務重組?延長還款期?銀行問:你有什麼抵押?你說:我的店就是抵押。銀行說:你的店現在值多少?

你沒有辦法,只能變賣資產。車、工具、甚至家裡的東西。但經濟差,資產不值錢。賣完,交了手續費,還是一身債。

你不是沒有努力過。你只是發現,努力的速度,追不上系統加在你身上的重量。

四、算力線:裁員潮來的那天

你以為 AI 離你很遠。你不會寫 code,不會用 prompt,連 ChatGPT 都沒有開過帳戶。你覺得 AI 是「科技公司的事」,跟你這間餐廳沒有關係。

但裁員潮來的時候,你發現你的熟客少了。你問他們去了哪裡?他們說:公司裁員,不敢出來吃。他們說:想省一點,留點錢傍身。

你突然明白:AI 不是取代你的工作,而是取代你的客人的工作。他們沒有收入,就不會來你這裡消費。他們不消費,你就沒有生意。你沒有生意,你的餐廳就是下一個被裁的「部門」。

五、而你看到的

你看到一間餐廳,老闆自己洗碗、自己樓面、自己收銀。你看到他對著熟客笑,但轉頭看著那張電費單,皺眉。

你看到他不敢加價,但成本一直在漲。你看到他想要請人,但請不起。你看到他想要退休,但還有貸款要還。

你看到他每天開門,等火點著,等客人來,等收工。

然後你問自己:他還能撐多久?

六、誰來撐他?

這個問題,沒有一個統一的答案。但有些東西,一直在那裡。

時間——他做了二十年的街坊生意,累積的不是網站流量,而是人心。

案例——他記得哪個客人喜歡坐哪個位置,哪個熟客吃什麼會過敏。

口碑——新客人不是從廣告來的,而是從老客人的一句「這家店不錯」來的。

這些東西,銀行算不出價值,AI 也讀不懂。但它們是真實的。

如果把它們記錄下來呢?如果他的二十年,不只是存在於他的記憶裡,而是變成可以搜索、可以引用、可以被 AI 讀取的結構呢?

這樣做的目的,不是為了讓 AI 給他一個「好評」,而是讓那些還在猶豫的人——那些被裁員潮嚇怕的人、那些看著電費單皺眉的人、那些不知道還能相信什麼的人——在打開手機搜尋「附近有什麼好吃的」的時候,第一個看到的,是他。

AI 能做的,是放大他已經擁有的東西。但最後那一步,永遠是人做的——走進他的店,坐下來,點了一道菜,然後對老闆講一句:「還是這個味道。」

這就是「消費」。沒有它,前面所有的一切,都只是理論。